How to get rid of credit card debt? As debt relief surges in popularity among Americans, a growing number of individuals embark on a quest to decipher the labyrinthine path toward qualification for this legal avenue of credit card debt obliteration. In the following discourse, we shall plunge headlong into the depths of wisdom, uncovering a trove of invaluable counsel, each a radiant beacon lighting the way to vanquish credit card debt. Remarkably, this venture may not necessitate the complete depletion of one’s financial reserves.

It is of paramount importance, indeed imperative, to judiciously select the most suitable institution offering an exemplary debt relief program. This discerning choice confers upon the debtor the capacity to promptly reconcile their debts, all while basking in the warm embrace of the most frugal interest rates. This chosen path represents a veritable conduit for the facile management of one’s financial obligations, a road unencumbered by onerous impediments.

Credit cards, those slender tokens of financial power, have the potential to metamorphose into veritable lifelines in times of fiscal turmoil and exorbitant expenditures, provided they are wielded with sagacity. They furnish a convenient conduit for liquidating pecuniary dues, thereby facilitating seamless transactions. Yet, the undue proliferation of credit cards, an abundance propagated by zealous issuers, often ensnares the unsuspecting populace, engendering a reckless proclivity towards accumulating more than one can judiciously manage, thereby descending into the morass of indebtedness. Real-Time eCommerce Sales Data: The most accurate, real-time sales data on 300,000+ Shopify stores.

A subtle yet unmistakable omen arises when the edifice of credit card bills, hitherto reasonably surmountable, begins its ascent into the stratosphere of financial obligations, with each passing month bringing forth a Herculean task of settling these accounts in full. Such a situation, an economic harbinger, clamors for the cultivation of fiscal discipline, a discipline that becomes the lodestar in one’s quest for the annihilation of credit card debt.

The Expedition Toward Credit Card Debt Eradication

In contemplation of institutions purporting to dispense reputable debt relief services, an air of prudence should envelop one’s decision-making process. One potential avenue to explore lies in the utilization of a debt relief network, a network that, akin to a swift messenger, proffers a helping hand in the endeavor to pare down and ultimately expunge one’s debt.

Amid this intricate tapestry of financial dynamics, it becomes all too apparent that legitimate establishments, entities that have traversed the labyrinthine byways of legality to firmly entrench themselves, offer an alternative to the perils of accumulating debts destined to linger ad infinitum. Thus, the prudent path is to opt for legal recourse to settle one’s indebtedness, a path illuminated by the beacon of rectitude. Get matched with a Career Advisor and Mentor who will help you select and enroll in the right program for you.

The pantheon of scrupulous debt relief services unfurls a diverse array of legal settlement options, each a soothing balm to alleviate the pressing burden of debt repayment. Seek a stratagem that accelerates the process of debt dissolution while imposing a nominal monthly tribute.

The astute debtor must be discerning in their selection not only of a strategy that offers succor in managing the tribulations of debt but also in the punctilious fulfillment of their obligations. For, should they gain entry into a debt relief program but falter in rendering the stipulated monthly disbursements, the chains of indebtedness shall remain intact, and the promised relief a mere chimera. This underscores the indispensability of availing oneself of professional guidance to comprehend with lucidity the intricacies of legally expunging credit card debt.

Divergent Paths for Divergent Debts

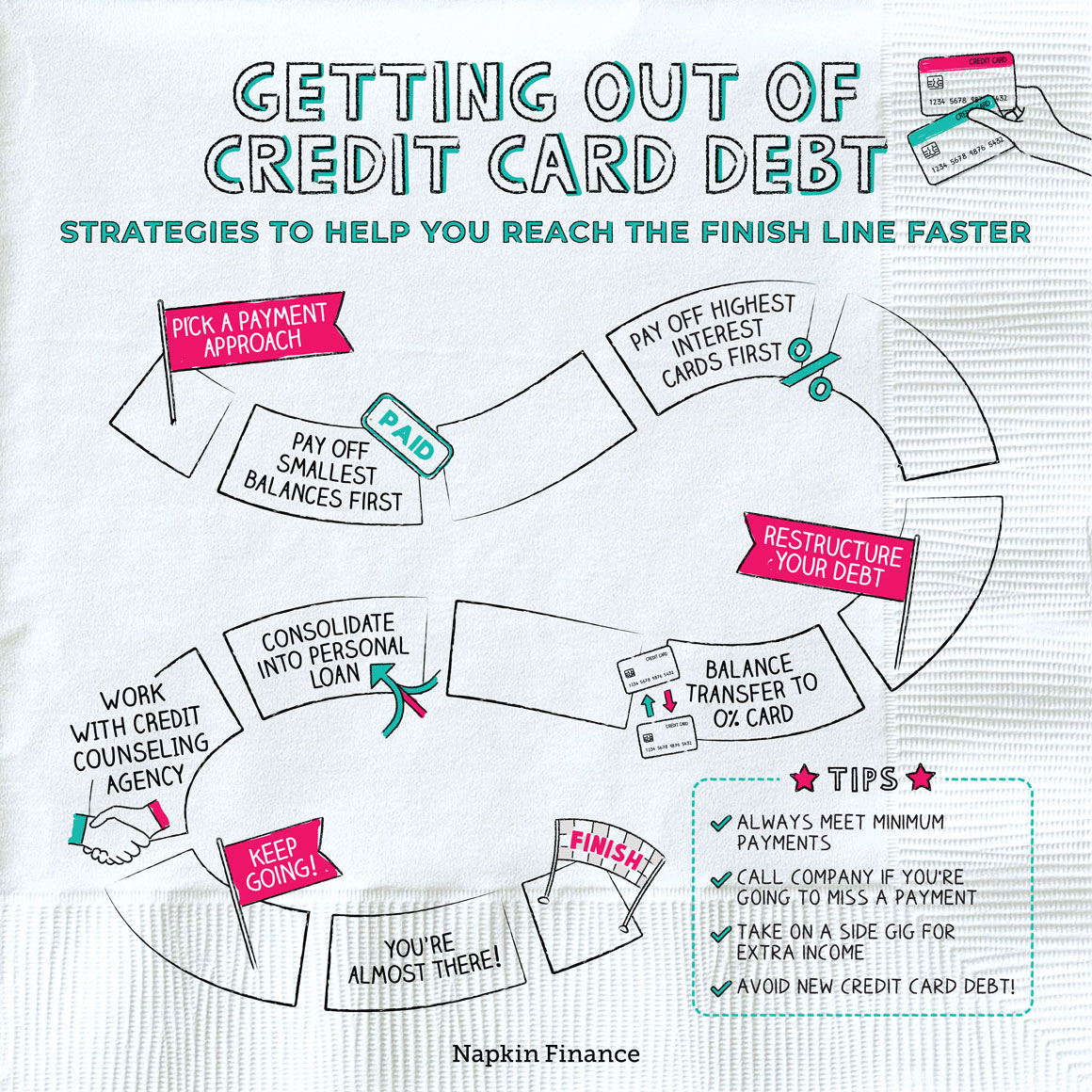

As we navigate the labyrinthine pathways of debt elimination, it is prudent to discern that strategies to efface current credit card debts with impending deadlines diverge from those suited to long-term debts accrued primarily through credit card Equated Monthly Installments (EMIs). Herein, a compendium of seven elemental techniques emerges, each a facet of the multifaceted prism of debt eradication. Business – Money Making – Marketing – Ecommerce.

1. Pay As Much As You Can

In the event of difficulty securing the necessary funds to retire your credit card debts, defaulting on the total payment becomes an ominous possibility. However, this perilous course can lead to a mountainous debt burden due to the exorbitant APR (Annual Percentage Rate). Instead of remitting nothing or a mere minimum payment, the judicious choice is to remit the largest feasible amount. Such an approach assures that your subsequent statement will not be a ponderous millstone around your financial neck.

2. Apply for a Loan

Contemplating the procurement of a personal loan for the settlement of credit card bills demands prudent deliberation, as it carries the potential to ensnare you in a web of indebtedness. Should the interest on your credit card prove substantially higher than the interest on a personal loan, this avenue may warrant consideration. Nevertheless, it is incumbent upon you to borrow only the amount essential, resisting the temptation of a larger loan.

The timely remittance of loan Equated Monthly Installments (EMIs) assumes paramount importance to forestall adverse impacts on your credit score. For those in possession of valuable assets like property or securities, eligibility for secured loans such as Loans Against Property or Loans Against Securities presents itself. Yet, instead of mortgaging these assets as collateral, contemplate their liquidation should they no longer yield the desired returns.

3. Seek Help from Friends and Family

When faced with dire financial exigencies, seeking a diplomatic overture with friends and family is warranted. Borrowing funds from close acquaintances offers immediate liquidity while sparing you the onerous encumbrance of usurious interest rates. To fortify these familial bonds, it is prudent to discharge these debts prior to the mutually agreed-upon deadline, thus averting potential rifts.

4. Balance Transfer

In the event of a substantial credit card debt looming large on the imminent billing horizon, the option of balance transfer warrants consideration. This artful stratagem entails migrating the outstanding debt from one or more credit cards to another endowed with this fiscal feature. This transmigration confers an additional respite, typically spanning 45 to 90 days, for the redemption of the transferred debt, contingent upon the issuer’s terms and the intricacies of your billing cycle.

This hiatus offers the opportunity to orchestrate your financial affairs, thereby expediting the timely liquidation of debts. However, one must exercise caution, for failure to discharge the dues even within this interest-free interregnum may culminate in the imposition of the standard APR (Annual Percentage Rate). How AI, ChatGPT maximizes the earnings of many people in minutes.

5. Negotiate with Your Credit Card Company

In times of financial turmoil, a diplomatic overture to your credit card company is warranted. Whether felled by job loss, beset by a medical exigency, or ensnared in the throes of other legitimate crises, communication with the credit card issuer is the prudent course. Plead your case, elucidate the extenuating circumstances, and beseech them to lower the prevailing interest rate, particularly if you bear a laudable history with the institution.

6. Prioritize Payments

The ordering of payments assumes paramount importance when navigating the labyrinthine labyrinth of debt. The catalog of debts, replete with due dates, Annual Percentage Rates (APR), and the allotment of available resources, necessitates a methodical approach. While conventional wisdom dictates the prioritization of debts based on due dates, a more judicious strategy may entail categorizing debts in accordance with APR.

Consequently, the debt bearing the highest APR ascends to the zenith of priority, affording respite from burgeoning interest costs. Should the debts bear similar APRs, the stratification then hinges on the outstanding balance, with the smaller sum receiving priority.

7. Convert Payments to EMIs

Credit cards, versatile instruments of fiscal prowess, bestow upon their bearers the ability to transmute monumental expenditures and monthly credit card obligations into manageable Equated Monthly Installments (EMIs). Suppose, for instance, that an acquisition, be it a smartphone or an amalgam of transactions amassing to $1,000, is consummated with a credit card.

This veritable treasure trove of transactions can be converted into a series of EMIs, thereby circumventing the burdensome exigency of immediate payment. Nevertheless, the discerning debtor must proceed with circumspection, for credit card companies typically impose annual interest rates ranging from 12% to 36% for EMIs, often accompanied by a processing fee spanning 1% to 3% of the outstanding sum.

Charting the Course for Long-Term Credit Card Debt Management

In the annals of credit card debt management, seven elemental strategies emerge, each a sentinel guarding against the resurgence of debt and heralding the path toward fiscal redemption. Loans & Financial Services for Business or Personal Purposes.

The initial sojourn on this odyssey toward financial emancipation may necessitate the enlistment of professional counsel. For those grappling with colossal debts and finding conventional methods, the sage advice of financial professionals or consultants may serve as the guiding star illuminating the path to a debt-free horizon. It is incumbent upon the debtor to fathom that these financial sages are akin to benevolent physicians, prepared to dispense aid sans the gavel of judgment, provided they are furnished with precise information.

A cardinal error in the voyage toward debt annihilation is the satisfaction of only the minimum due on credit card bills. This seemingly innocuous act conceals a perilous chasm, for the issuer, while not deeming it a default, exacts a prohibitive interest rate on the remaining balance. Thus, a single dalliance with the minimum payment serves as the harbinger of augmented debt in the ensuing billing cycle. Ideally, the debtor ought to endeavor toward the payment of credit card bills in their entirety. In the absence of this ideal, remittance exceeding the minimum due emerges as the judicious recourse, conferring respite from the clutches of exorbitant interest.

The cultivation of fiscal discipline, akin to the nurturing of a verdant garden, represents the panacea for those grappling with the exigencies of monthly credit card bills. In such instances, introspection becomes paramount. Shearing off expenses that lean toward luxury or deferrable acquisitions becomes a prescient measure. The reduction in the number of credit cards in one’s possession, should they prove unwieldy to manage, is a prudent gambit.

The advent of the auto-pay feature on the credit card serves as an invaluable sentinel against the scourge of tardy payments. With its activation, payments are automatized and debited with unwavering regularity from the registered bank account on the due date. The implementation of this feature, akin to a vigilant guardian, obviates the ignominious consequences of procrastination.

The bazaar of credit cards, a veritable emporium teeming with choices, evokes imagery of a vast sea bespeaking myriad possibilities. While many are ensnared by the siren call of features, bonuses, and reward points, those ensconced in the tumultuous sea of monthly expenditures, buffeted by an absence of fiscal restraint, would be prudent to steer their course toward a credit card endowed with a low Annual Percentage Rate (APR). This financial compass augments the capacity to mollify interest in instances where complete repayment remains elusive. Loans & Financial Services·Credit Cards·Reporting & Repair·Tax· Insurance· Legal· B2B.

The edifice of fiscal redemption is constructed upon the bedrock of an affordable budget, a budget that plots the course toward achievable objectives. The meticulous scrutiny of spending habits gives rise to the delineation of limits on credit card expenditure. The curtailment of extravagant expenses, while arduous in its nascent stages, is an endeavor that reaps dividends in the quest for debt emancipation. In the ceaseless endeavor to restrain spending, the prospective debtor may avail themselves of the facility to diminish their credit card spending limit through online banking or their credit card account. For those still grappling with profligate spending, the augmentation of income through supplementary employment emerges as an efficacious strategy, facilitating swifter debt repayment.

The formulation of a repayment strategy, a strategy informed by a nuanced understanding of diverse debt management options, heralds the commencement of the final leg of the debt-elimination journey. Here, the confluence of all outstanding debts, including the specter of credit card debt, beneath a single, all-encompassing umbrella, emerges as a tactic that streamlines the tracking of payments, obviating the prospect of missed Equated Monthly Installments (EMIs). The avenue of debt consolidation looms large, potentially ushering forth a reduction in interest expenses. Those grappling with a constellation of diminutive debts, debts too modest to countenance the burden of repayment, may contemplate the avenue of a ‘personal loan for debt consolidation.’ Furthermore, the vista of secured loans, including ‘Loan Against Property’ or ‘home refinancing,’ beckons as a potent means of debt obliteration. This stratagem, known as the debt consolidation loan, amalgamates a multitude of debts into a solitary Equated Monthly Installment (EMI) replete with a diminished interest rate and extended repayment tenures, all of which culminate in a reduction in monthly outlays. It is noteworthy, however, that the speedy payment of the debt consolidation loan is advised, for this course of action ushers forth savings on interest. Conversely, ‘personal loans for debt consolidation’ remain ensconced in the realm of higher interest rates, best suited for situations poised on the precipice of financial peril. Mindful Trader: Loans. Financial Services.Gifts. Stock Picking.

3 Methods for credit card debt obliteration

In the labyrinth of credit card debt obliteration, an array of methods unveils itself:

- The Avalanche Method is a stratagem predicated upon the payment of the minimum due on all credit card bills while allocating the maximum sum to the card encumbered with the most elevated Annual Percentage Rate (APR). This tactic, akin to a financial chess move, serves to mitigate interest costs in instances of tardy payments.

- The Snowball Method, akin to a financial alchemical transformation, sees the payment of the minimum due on all credit card bills, with the maximum allocation directed toward the card burdened by the most modest balance. This stratagem, predicated upon the principle of incremental victories, galvanizes the rapid eradication of debts.

- The Blizzard Method, an amalgamation of the Avalanche and Snowball Methods, first entails the payment of the smallest debt before contending with the card encumbered by the highest interest rate. This stratagem, akin to a financial tempest, combines elements of tactical precision with the momentum of incremental victories.

In the denouement, the achievement of a successful debt settlement hinges upon the creditor’s acquiescence to the reduction of the debt by a specified quantum, a concession typically engendered through negotiations conducted by a debt settlement company. Ergo, the selection of the right institution, one replete with acumen and expertise, assumes paramount importance, lest the debt remain obstinately impervious to erasure.

The contours of debt settlement typically encompass unsecured debts. For those who have tendered their home or automobile as collateral, the threshold of eligibility for this program may remain elusive.

Final thought

The demarcation between spurious and genuine firms is, in most cases, a straightforward undertaking. Reputable companies, those institutions bedecked in the raiment of credibility, diligently adhere to the protocol of accumulating and disbursing funds through FDIC-insured accounts. In stark contrast, their illegitimate counterparts, ensnared in the quagmire of unscrupulousness, cast aside these sacrosanct standards. Loans & Financial Services·Real Estate·Legal·B2B.

In the antechamber of soliciting aid for the settlement of unsecured debts, it is incumbent upon the debtor to embark upon an expedition to fathom their rights. The acquisition of the knowledge requisite for the eradication of credit card debt serves as a bulwark against the pitfalls of perpetuating fiscal tribulations.